23

Jun

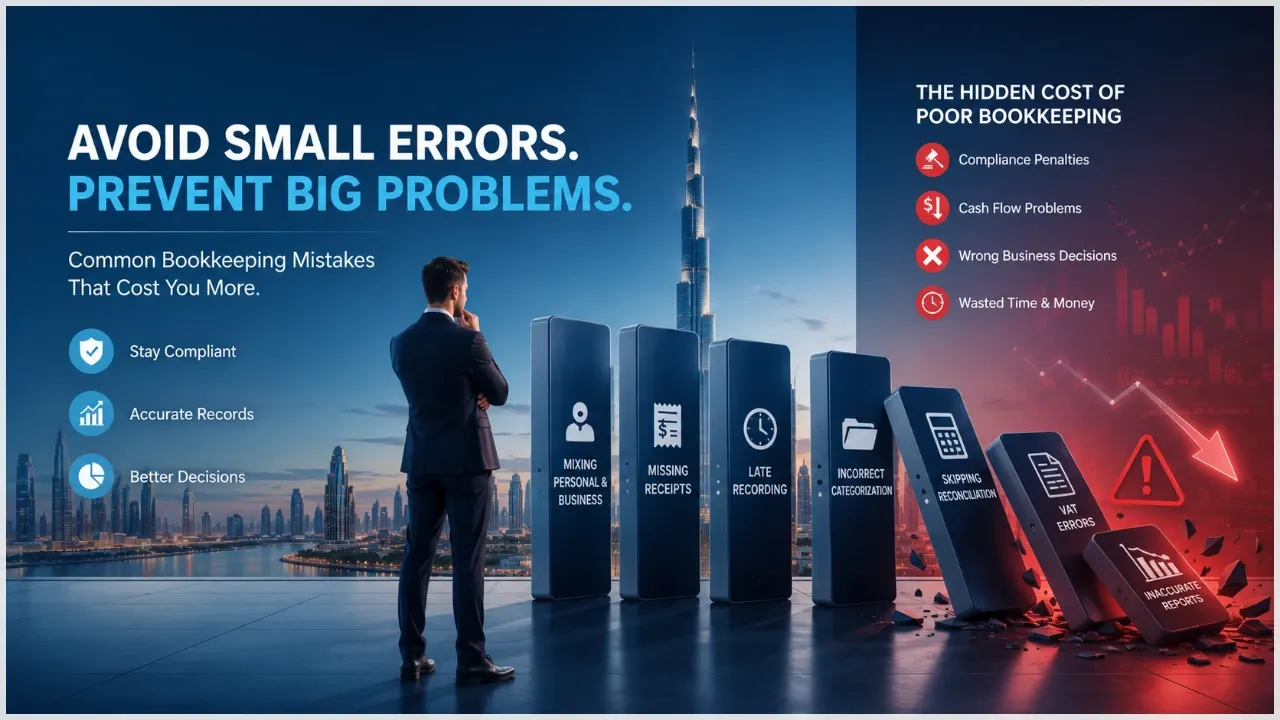

Bookkeeping Mistakes: Common Accounting Errors to Avoid

Bookkeeping is much more than recording income and expenses. It provides the financial foundation that helps businesses monitor performance, manage cash flow, comply with UAE regulations, and make informed decisions.

Unfortunately, many businesses make common bookkeeping mistakes that seem minor at first but can create major problems later. Missing invoices, incorrect expense classifications, delayed record updates, and poor documentation can lead to compliance issues, inaccurate financial reports, VAT filing errors, and unnecessary rework.

Whether you manage your own books or work with professional accounting services Dubai, understanding these common accounting mistakes can save your business significant time, money, and stress.

This guide explains the bookkeeping errors that businesses frequently make, why they happen, and the best ways to avoid them.

Why Accurate Bookkeeping Matters

Every financial decision depends on accurate records.

Proper bookkeeping helps businesses:

- Monitor profitability

- Track expenses

- Prepare financial statements

- Meet VAT and Corporate Tax obligations

- Improve budgeting

- Support audits

- Make confident business decisions

Poor bookkeeping affects every part of a business—not just the accounting department.

Mistake 1: Mixing Personal and Business Expenses

One of the most common bookkeeping mistakes is using the same bank account or credit card for both business and personal spending.

Examples include:

- Paying personal shopping bills from the business account

- Using company funds for family expenses

- Depositing personal income into the business account

Why It Creates Problems

Mixed transactions make it difficult to:

- Calculate business profit

- Track deductible expenses

- Prepare tax reports

- Complete audits

How to Avoid It

- Open a dedicated business bank account.

- Use separate business payment cards.

- Record owner withdrawals correctly.

Mistake 2: Waiting Too Long to Record Transactions

Many businesses postpone bookkeeping until the end of the month—or even the end of the financial year.

By then:

- Receipts may be lost.

- Transactions are forgotten.

- Bank reconciliations become difficult.

Practical Example

A restaurant records hundreds of daily transactions. Waiting several weeks before updating records makes it almost impossible to identify missing payments.

Best Practice

Record transactions daily or at least weekly.

Mistake 3: Losing Receipts and Supporting Documents

Bookkeeping is not only about numbers—it also requires evidence.

Businesses often lose:

- Purchase invoices

- Fuel receipts

- Utility bills

- Supplier invoices

- Customer receipts

Without supporting documents, expenses may become difficult to verify during audits.

How to Avoid It

- Scan receipts immediately.

- Store digital copies securely.

- Organize documents by month.

Mistake 4: Incorrect Expense Categorization

Not every payment belongs in the same expense category.

Examples of incorrect classification include:

- Recording equipment purchases as office supplies

- Treating loan repayments as expenses

- Recording owner's drawings as salaries

Incorrect categorization produces misleading financial reports.

Best Practice

Use a well-structured chart of accounts and consistent accounting categories.

Mistake 5: Skipping Bank Reconciliation

Bank reconciliation compares your accounting records with your bank statements.

Businesses that skip this step often miss:

- Duplicate payments

- Bank charges

- Missing deposits

- Recording errors

- Unauthorized transactions

Practical Example

A customer transfers payment twice. Without reconciliation, the duplicate transaction may remain unnoticed.

Monthly reconciliation helps detect issues early.

Mistake 6: Ignoring Small Transactions

Some business owners believe small expenses are insignificant.

Examples include:

- Parking fees

- Office snacks

- Courier charges

- Minor repairs

- Taxi fares

Although individually small, these expenses add up over time and affect profitability.

Every legitimate business transaction should be recorded.

Mistake 7: Missing Sales Invoices

Every sale should have supporting documentation.

Common problems include:

- Forgotten invoices

- Duplicate invoices

- Missing invoice numbers

- Incorrect invoice amounts

Missing sales records affect revenue reporting and VAT calculations.

How to Avoid It

Use accounting software that generates sequential invoice numbers automatically.

Mistake 8: Poor Inventory Tracking

Businesses selling physical products often struggle with inventory management.

Common errors include:

- Unrecorded stock purchases

- Missing stock adjustments

- Incorrect stock valuation

- Inventory shortages

Poor inventory records result in inaccurate profit calculations.

Practical Example

A retail business sells products without updating inventory, making financial reports show stock that no longer exists.

Mistake 9: Delayed Payroll Recording

Payroll should be recorded accurately every pay period.

Common mistakes include:

- Missing salary payments

- Incorrect overtime calculations

- Unrecorded bonuses

- Payroll timing differences

Payroll errors affect both employees and financial statements.

Maintain complete payroll records every month.

Mistake 10: VAT Recording Errors

VAT mistakes are among the most serious bookkeeping issues for UAE businesses.

Examples include:

- Recording VAT incorrectly

- Missing tax invoices

- Claiming ineligible input VAT

- Using incorrect VAT rates

- Forgetting VAT adjustments

Best Practice

Maintain organized VAT records and review transactions regularly before filing returns.

Mistake 11: Poor Corporate Tax Record Keeping

Corporate Tax compliance relies heavily on accurate bookkeeping.

Missing financial records may create problems during:

- Tax calculations

- Financial reporting

- Audit preparation

- Compliance reviews

Good bookkeeping supports accurate Corporate Tax reporting from the beginning.

Mistake 12: Duplicate Entries

Entering the same transaction twice is more common than many businesses realize.

Duplicate entries may occur when:

- Multiple employees record the same payment.

- Bank imports are duplicated.

- Manual entries are repeated.

Duplicate transactions distort:

- Revenue

- Expenses

- Cash balances

- Financial reports

Regular account reviews help identify duplicate entries quickly.

Mistake 13: Not Backing Up Financial Data

Many businesses rely entirely on a single computer.

If hardware fails or files become corrupted, years of financial information could be lost.

Best Practice

Maintain:

- Cloud backups

- External hard drive backups

- Secure accounting software backups

Financial records should always be protected.

Mistake 14: Ignoring Outstanding Receivables

Sales alone do not improve cash flow.

Businesses should regularly monitor:

- Unpaid customer invoices

- Overdue payments

- Credit limits

- Collection status

Poor receivable management creates unnecessary cash flow problems.

Mistake 15: Not Reviewing Financial Reports

Some businesses prepare financial reports but never review them.

Important reports include:

- Profit and Loss Statement

- Balance Sheet

- Cash Flow Statement

- Accounts Receivable Report

- Accounts Payable Report

Reviewing these reports helps identify issues before they become serious problems.

Mistake 16: Using Outdated Accounting Processes

Manual spreadsheets may work for very small businesses, but growing companies often benefit from modern accounting software.

Modern bookkeeping software offers:

- Automatic bank feeds

- Invoice management

- VAT reporting

- Financial dashboards

- Cloud access

- Better data security

Automation also reduces manual errors.

Mistake 17: Trying to Handle Everything Alone

Many entrepreneurs attempt to manage bookkeeping themselves while also running the business.

As the business grows, bookkeeping becomes more complex.

Professional bookkeeping services can assist with:

- Monthly bookkeeping

- Financial reporting

- VAT preparation

- Corporate Tax support

- Payroll records

- Compliance documentation

Outsourcing bookkeeping often saves both time and money.

Warning Signs Your Books Need Attention

Watch for these common warning signs:

- Missing receipts

- Negative cash balances

- Unexplained bank differences

- Unpaid invoices increasing

- Frequent bookkeeping corrections

- Late VAT filings

- Financial reports that don't match business activity

These issues usually indicate bookkeeping needs immediate review.

Best Practices for Accurate Bookkeeping

Follow these habits to keep your books clean and compliant:

- Record transactions regularly.

- Separate business and personal finances.

- Reconcile bank accounts every month.

- Keep digital copies of all invoices and receipts.

- Review financial reports monthly.

- Monitor outstanding customer payments.

- Maintain organized VAT records.

- Back up financial data securely.

- Use reliable accounting software.

- Work with experienced bookkeeping professionals when needed.

Small improvements today prevent major accounting problems tomorrow.

Conclusion

Bookkeeping mistakes rarely happen because businesses intend to keep poor records. More often, they result from busy schedules, inconsistent processes, or a lack of financial organization. Unfortunately, even small errors can create larger issues, including inaccurate reports, compliance risks, delayed VAT filings, and unnecessary rework.

By keeping financial records up to date, organizing supporting documents, reviewing reports regularly, and following sound bookkeeping practices, businesses can improve financial accuracy and reduce compliance risks.

Whether you're a startup or an established company, investing in accurate bookkeeping is one of the smartest decisions you can make for long-term business success.

Frequently Asked Questions

1. What is the most common bookkeeping mistake?

Mixing personal and business expenses is one of the most common bookkeeping mistakes and can make financial reporting and tax compliance much more difficult.

2. Why is bank reconciliation important?

Bank reconciliation helps identify missing transactions, duplicate entries, bank charges, and recording errors before they become larger financial problems.

3. How often should bookkeeping records be updated?

Businesses should ideally record transactions daily or weekly and reconcile accounts every month to maintain accurate financial records.

4. Can poor bookkeeping affect VAT and Corporate Tax compliance?

Yes. Inaccurate bookkeeping can lead to incorrect tax calculations, filing errors, delayed submissions, and additional compliance risks.

5. Should small businesses hire professional bookkeeping services?

Many small businesses benefit from professional bookkeeping services because they improve financial accuracy, save time, and help ensure compliance with UAE regulations.

Keep Your Books Accurate and Your Business Compliant

Avoid costly bookkeeping mistakes with professional support. Our experienced team helps businesses maintain accurate financial records, prepare compliant reports, manage VAT and Corporate Tax requirements, and keep your accounts organized throughout the year.

Talk to Our Bookkeeping Experts